Top 10 Takeaways from SIFMA’s Economist Roundtable Year-End Survey

- Published on:

- December 12, 2022

- By:

- Katie Kolchin, CFA

- Katie Kolchin

Everything You Need to Know about Inflation, Rates, and Recession

In SIFMA’s semiannual economic surveys (published every June and December), we ask our Roundtable of economists to provide their best assessment of the current economic environment and where we could be headed.

Recently, we published our 2022 year-end survey. Our economists estimated 2022 GDP growth at +0.3% (median forecast, 4Q/4Q), followed by -0.3% for 2023. 83% of economists expect a long-term potential GDP growth rate of 1.5-2.0%, with 64% stating this is unchanged from pre-COVID estimates. The main factors impacting economic growth were identified as:

- For 2022: inflation, tight labor market, and U.S. monetary policy

- For 2023: U.S. monetary policy, inflation, and recession threat

Unless you are living at McMurdo research station in Antarctica, you most likely are discussing inflation on a daily basis. At levels not seen since the 1980s, people are feeling inflation everywhere. Markets are ebbing and flowing – mostly in the downward direction – based on inflation reports. And, importantly, the Fed is basing its monetary policy on inflation data.

Listen to this post. Katie Kolchin talks through the top 10 takeaways from SIFMA’s year-end economic survey. Enjoy more audio and podcasts on Apple Podcasts and Google Podcasts.

In this survey, we dug in on inflation, rates, and recession. The report also includes a breakdown of the components of inflation – supply side, demand side, and the labor component – and when pressures on each of these components could dissipate.

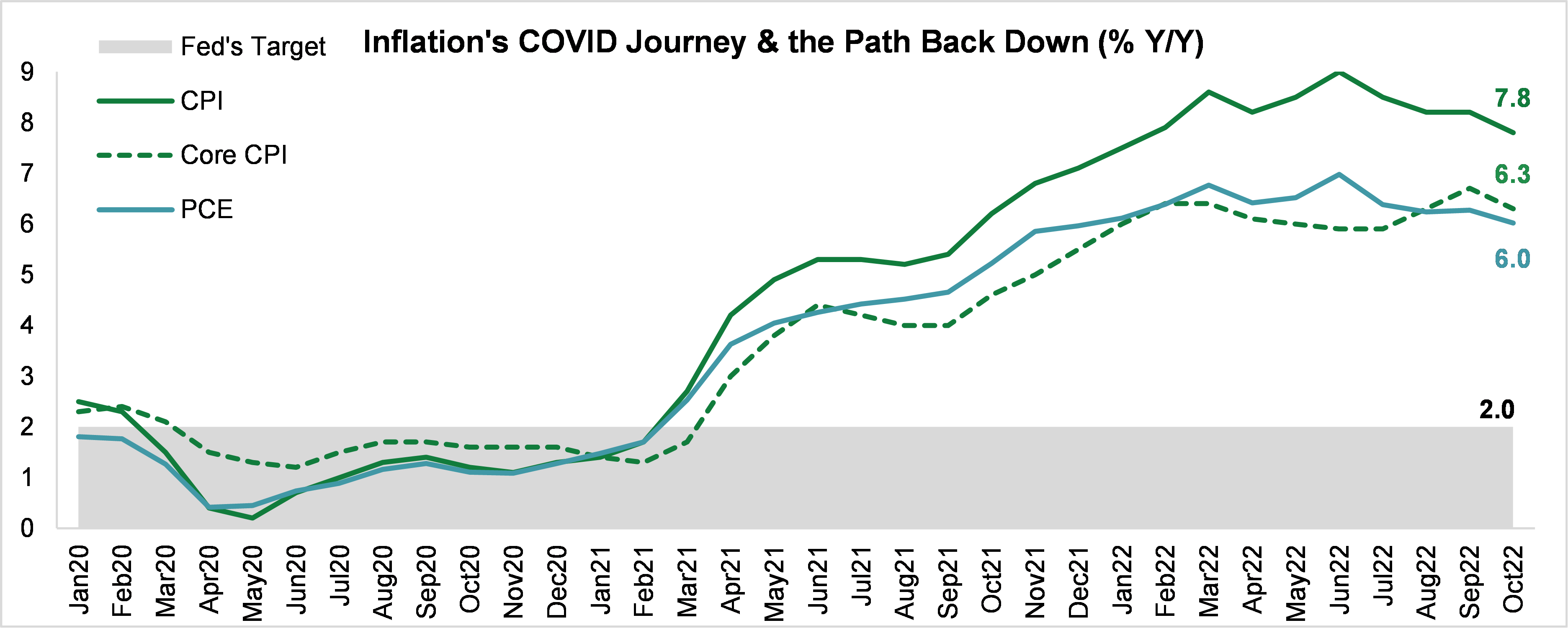

To begin, we recapped where we are in inflation and the path back down to the Fed’s 2% target. The PCE – the Fed’s preferred inflation measure and the one typically used to set monetary policy – remained elevated at +6.0% in October. This was down from the 7.0% peak in June but +4.0 pps to the target.

Source: FRED, SIFMA estimates

Source: FRED, SIFMA estimates

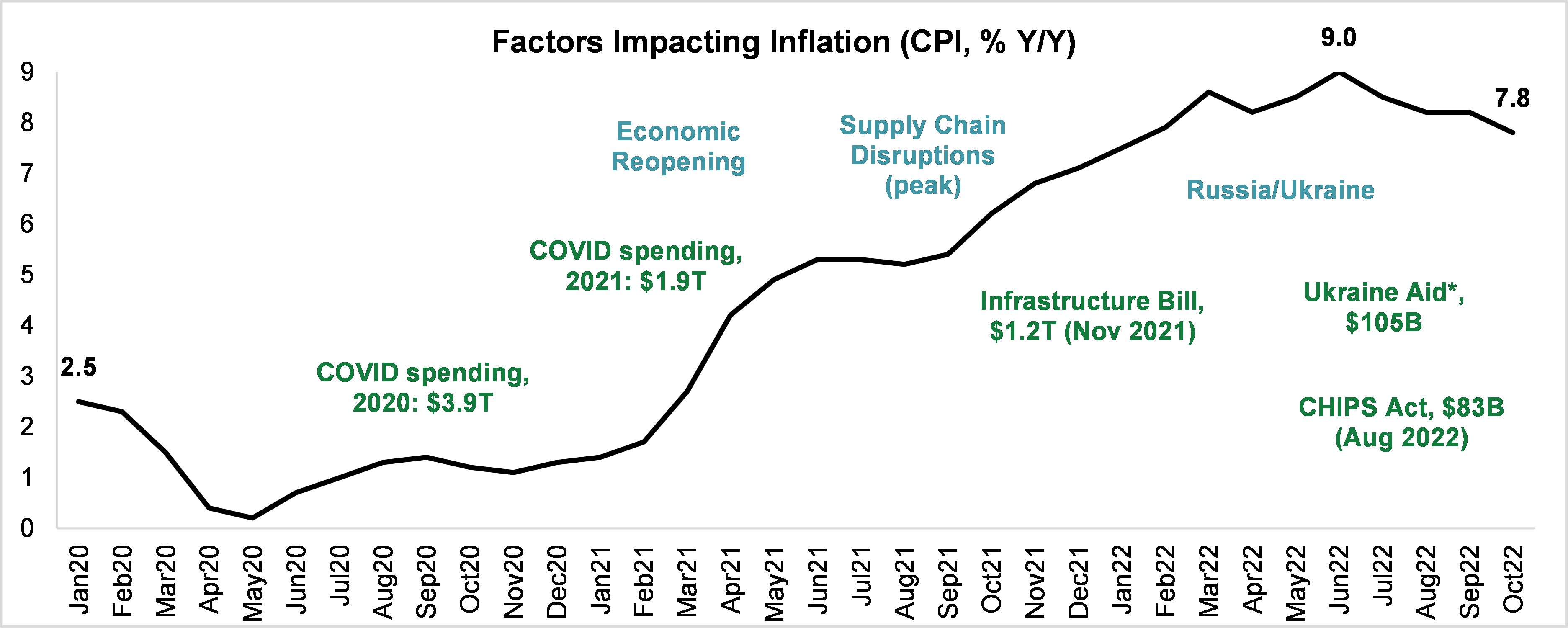

We then reminded readers how we got to these inflation levels, since many different factors drove the increase in inflation, not all of which can be impacted by monetary policy.

- Fiscal spending, >$7 trillion since March 2020: COVID associated, administration policies, Ukraine aid

- Other factors: post-COVID economic reopening, supply chain disruptions, Russia/Ukraine war

- Monetary policy (not depicted graphically): +$4.4 trillion added to the Fed’s balance sheet since March 2020

Source: FRED, IMF, SIFMA estimates Note: Ukraine Aid includes $37.7B the administration requested on November 15

Source: FRED, IMF, SIFMA estimates Note: Ukraine Aid includes $37.7B the administration requested on November 15

Finally, we highlight the top ten survey results from our Roundtable economists:

Inflation

#1. 75% of respondents believe price pressures are at their peak – PCE estimated to end 2022 at +5.8% and end 2023 at +2.9% – but will remain elevated for some time, with 55% responding inflation will not reach the Fed’s preferred 2% target until beyond 2024

#2. Ranking the factors having the biggest impact on the aggregate inflation rate in order, economists replied: (1) demand side, (2) supply side, and (3) the labor component

#3. Ranking supply side inflation components, economists replied: domestic supply chain issues (port congestion, labor shortages), commodity price shocks (oil due to Russia/Ukraine war), and supply chain issues (China’s zero COVID policy)

#4. Ranking demand side inflation components, economists replied: consumer spending on services, consumer spending on goods, and fiscal spending

#5. Labor component: 80% of respondents believe we are not in a wage-price spiral, with 72% of respondents believing we have reached a peak in wage pressures

#6. No respondents believe inflation expectations are unanchored, and no respondents expect inflation expectations will become unanchored

Rates

#7. 46% of respondents expect the peak Fed Funds rate will be 500-550 bps, with 92% of respondents expecting the peak rate to be achieved by mid-2023

#8. 58% of respondents think the Fed should pause and assess the impact of earlier rates hikes, with 50% of respondents indicating this pause should take place in 2Q23

Recession

#9. None of the respondents believe the U.S. is already in a recession, while 83% of respondents believe the U.S. will enter a recession

#10. If the U.S. enters a recession, 89% of respondents believe it will be mild and 60% of respondents believe it will occur in 1H23

—

Katie Kolchin, CFA, is a Managing Director and Head of SIFMA Research. She is also the author of SIFMA Insights.